Mortgage financing made easy

Debra Parker. Canadian Mortgage Expert.

Serving clients in BC from my office in Cranbrook.

Finding the best mortgage can be frustrating. It doesn't have to be when you follow my 3 step plan.

Get started right away

The best place to start is to connect with me directly. My commitment is to listen to your needs, assess your financial situation, provide professional mortgage advice, and

guide you through the mortgage process.

Get clarity

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming.

Let me cut through the noise. I'll outline the best mortgage products available with your needs in mind.

Proceed with confidence

My goal is to make sure you know exactly where you stand at all times. From your initial application through your mortgage renewal, I'm available to answer any questions for as long as you need a mortgage.

I've got you covered.

Hi, I'm Debra, and I'm passionate about helping my clients find the best mortgage products to suit their unique needs. I've been in the mortgage industry since 2006, and prior to that, I spent 12 years as an Assistant Manager with a consumer finance company. This experience has given me a diverse skill set that allows me to accurately assess my client's needs and guide them through every step of the mortgage process.

As your mortgage professional, I make your interests my top priority. I'm committed to staying in touch with you throughout the term of your mortgage, and I'll work with you to ensure that you receive the best mortgage and the best rate when the term comes due. I believe that arranging your mortgage is just the beginning of our relationship, and I'm dedicated to providing ongoing support and guidance to my clients.

I grew up in the Kootenays, and I've spent most of my life in the area. While I'm away from the office, I love spending time travelling and enjoying outdoor activities with my friends and family. I'm also an avid cyclist and have achieved several athletic milestones, including setting a Canadian Powerlifting Record in the Bench Press in 2006 and winning the BC Provincials and Canadian National Masters Road Race and TT Championships in 2019.

It would be my pleasure to work with you, so please don't hesitate to get in touch if you have any mortgage-related questions or needs.

Nice things people have said about working with me.

Everything you need,

all in one place

As a trusted mortgage provider, let me help you with these services.

Click through any of the services to learn more

Canadian Mortgage Experts has partnered with APOLLO, Canada’s leading online provider of personal & business insurance, to provide exclusive home and condo insurance offers.

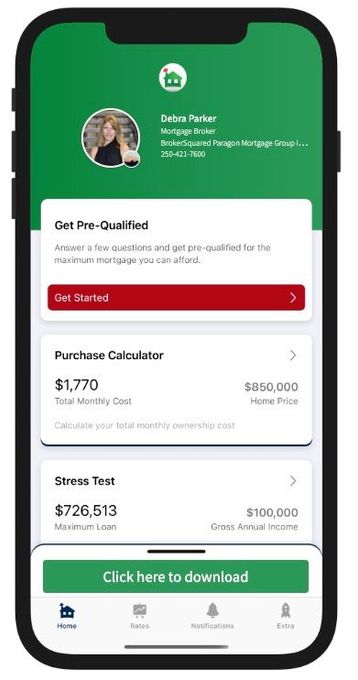

Download my Canadian Mortgage App

What you can do with my app

Calculate your total cost of owning a home

Estimate the minimum down payment you need

Calculate Land transfer taxes and the available rebates

Calculate the maximum loan you can borrow

Stress test your mortgage

Estimate your Closing costs

Compare your options side by side

Search for the best mortgage rates

Email Summary reports (PDF)

Use my app in English, French, Spanish, Hindi, and Chinese

Get started by completing my online mortgage application.

I'll let you know exactly where you stand so you can proceed with confidence.

Go ahead and schedule a meeting with me!

Mortgage articles to keep you informed.